The plot vs house investment Pakistan debate is the second-most-common question in Pakistani property forums. The honest answer is: it depends entirely on your time horizon, liquidity needs, and tolerance for active management. This guide walks through the real numbers — return profile, holding cost, liquidity, financing access — and gives you a clear decision framework.

The return profile, explained simply

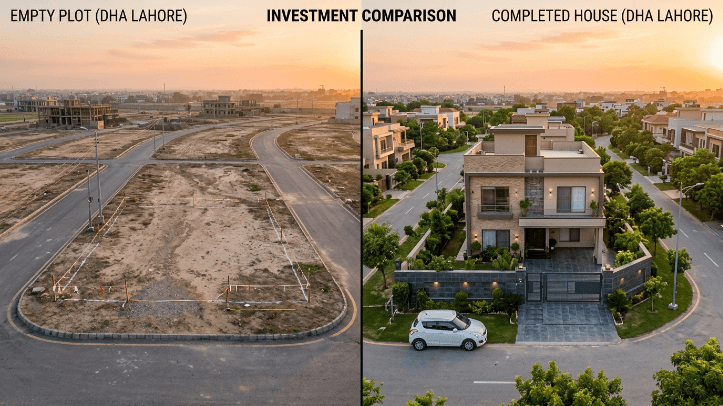

Plots are pure land bets. Your only return is capital appreciation. Zero cash flow during the hold (no rent). Holding cost is minimal: just property tax and a small annual society fee.

Houses are productive assets. You get capital appreciation PLUS rental income during the hold. But holding cost is higher: property tax, maintenance, vacancy gaps, property management fees if you outsource.

Over a 10-year hold in DHA Lahore, the math typically works out like this:

| Investment | Capital appreciation (10-yr CAGR) | Annual cash yield | Total return |

|---|---|---|---|

| 10-marla plot (DHA Phase 6, undeveloped) | 11 — 14% | 0% | ~12% IRR |

| 10-marla house (DHA Phase 5, rented) | 8 — 10% | 4.5 — 6% | ~12% IRR (similar) |

The total returns end up similar. The difference is when the return shows up — plots back-load it into a single exit event; houses spread it across years.

Where plots win

1. New societies launching today

Plots in newer societies (DHA Defence Raya, Etihad Town, Bahria Orchard) have 3-5x appreciation potential over 10 years if the society reaches full development. The trade-off: 30-50% chance of underperformance if the society stalls. This is why early-stage plot investing is a higher-variance bet.

2. Capital growth phases (3-5 year holds)

When the market is in a growth cycle (broadly 2014-2017, 2021-2022 in Lahore), plot appreciation outpaces house appreciation by 2-4 percentage points annually. The reason: limited new supply + speculative buying pile into the easiest-to-trade asset (plots).

3. Low-management investors

If you live overseas, plots eliminate the headache of finding tenants, managing maintenance, handling vacancy. Pay the annual property tax, wait, sell.

Where houses win

1. Income matters

If you need cash flow during the hold (retirement, supplementing salary), houses are the only option. A PKR 5 crore house produces PKR 25-30 lac annual rent. A PKR 5 crore plot produces zero.

2. Bank financing for purchase

Pakistani banks lend against built-up houses, not against plots. If you need 50-65% of purchase price on a bank loan, houses are the path. Plot loans exist but are restricted to specific approved schemes and capped at 30-40% LTV with shorter tenor.

3. Defensive in down markets

Rental income provides a floor in down markets. When prices stagnate (broadly 2018-2020, 2023-2024), house investors still collect rent. Plot investors collect nothing and watch the value tread water.

Where plots can go wrong

The two most common plot mistakes:

-

Buying in a non-launched / un-developed society. Many "Phase 9" or "Phase 12" extensions of established names exist only on paper. The land may not be fully acquired. Roads, gas, electricity may be 10 years away. Verify development status by visiting the actual location, not by looking at the brochure.

-

Buying into an oversupplied launch. When a society launches with 20,000 plots and only 3,000 sell to end-users, the resale market becomes investor-vs-investor. Prices stay flat for years until end-user demand catches up.

The decision framework

Buy a plot if:

- Your hold horizon is 5+ years

- You don't need cash flow during the hold

- You have full purchase price in cash (no bank financing needed)

- You can stomach a 30% chance the asset underperforms by year 5

Buy a house if:

- You need cash flow during the hold OR you plan to live in it

- You need bank financing for more than 30% of purchase

- You want lower variance / more predictable return profile

- You can tolerate ongoing management work (or pay for it)

Buy both if your portfolio is large enough — a house for cash flow stability + a plot for capital growth optionality. The mix smooths volatility across market cycles.

For Lahore-specific yield benchmarks across societies, see our Rental yields in Lahore 2026 guide. For broader pricing across societies, see the Lahore property prices 2026 market report.

Verified Data Update (May 2026)

Based on OpenHouse.pk's verified active and sold inventory as of May 2026 — every row physically inspected, sentinel-price outliers removed:

| Society | Size band | P25 — P75 asking | Verified median | Sample size |

|---|---|---|---|---|

| DHA Lahore (all phases) | 5-marla | PKR 2.75 — 3.30 cr | PKR 3.10 cr | 246 |

| DHA Lahore (all phases) | 10-marla | PKR 5.13 — 6.50 cr | PKR 5.93 cr | 142 |

| DHA Lahore (all phases) | 1-kanal | PKR 9.83 — 16.00 cr | PKR 12.00 cr | 343 |

Data refreshed nightly. For live verified inventory, browse openhouse.pk/listings.